Will the Silicon Valley Bank failure permanently alter the monetary tightening cycle ? - 13 march 2023

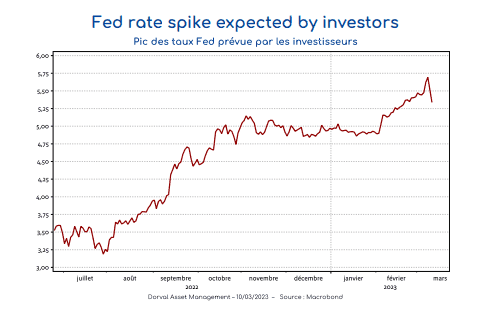

In recent weeks, investors have clearly been revising the monetary rate peaks in this cycle. Expectations were 5.5% in the United States and 4% in the Eurozone. There were two possible analyses. The first assessed that the majority of the US Federal Reserve's monetary tightening was behind us even if there was still uncertainty about the rate of the increase during the Federal Open Market Committee of 22 March (25 bp as in February or 50 bp?). In this case, it all comes down to prices and we must focus on a world where monetary rates will either remain unchanged or fall. Asymmetry is therefore positive for risk. The second concerned the non-linearity of rate hikes. Even if these rate hikes were limited and largely expected, they could lead to shocks in the economy or the financial system.

It is in this context that the setbacks of the small American bank SVB, which specialises in Silicon Valley startups, can be interpreted, in which it is a collateral victim of the rapid monetary tightening and bond crash of 2022. Another possible interpretation is more in relation to its business model as a deposit bank for startups, while the speculative bubble in this sector has been deflating for more than two years. At the very least, one can imagine that an episode of financial stress in the United States, even if limited, is likely to reduce the likelihood of a 50 bp rise in March. The FOMC could favour a more progressive approach (cf. chart 1).

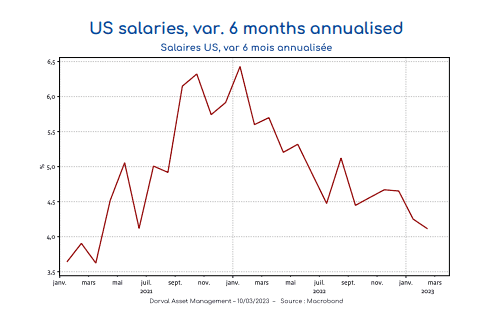

Macroeconomic data, for its part, blows hot and cold. While job creation in February was above expectations again (311k compared to expected 225k), the unemployment rate rose to 3.6% compared to the prior 3.4% and the hourly wage rose by only 0.2% compared to the expected 0.3% (cf. chart 2).

In our global flexible funds, a precautionary approach led us a few weeks ago to return to a near-neutral equity exposure and to increase option based hedging. We are maintaining this position in a delicate transition for risk.