Exposure rates of the Dorval Asset Management Range - January 09, 2023

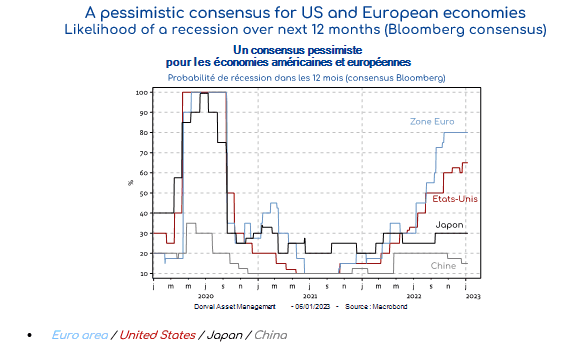

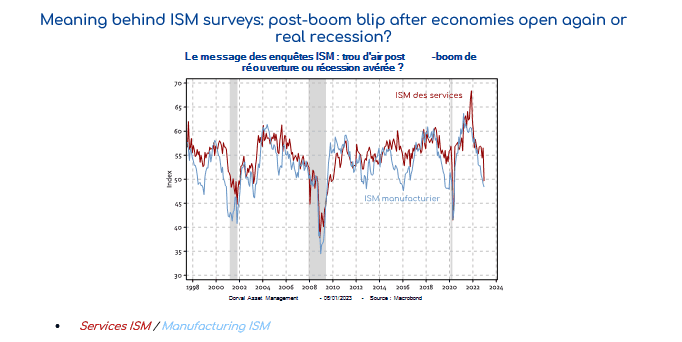

The consensus is expecting a recession this year, yet the latest economic statistics point to clear resilience in Europe. Looking across the pond, the situation in the United States is more of a mixed bag, as the labor market remains robust while ISM figures are plummeting. Yet inflationary pressure is clearly lessening, indicating that future monetary tightening is already broadly priced in. According to the latest Bloomberg consensus, the likelihood of a recession in the euro area and the US over the next 12 months is well above 50% (cf. chart 1). Some valid arguments support this scenario, and the sharp decline in the services ISM index in December (49.6) further bolsters them. In this scenario, US inflation would be swiftly reined in, and a new cycle would kick off: in this case, the dent for the equity markets resulting from a recession (decrease in profits) would be more than offset by clearer visibility resulting from the decrease in inflation and interest rates in our view. This is precisely what happened during the recessions in 1974 and 1991.

However, at this stage, a resilience scenario is equally possible in our view, given recent indicators pointing to ongoing positive momentum on the US labor market, with no acceleration in wages. It is therefore possible – but not definite – that weak survey data (PMI, ISM, cf. chart 2) reflect the end of the boom in orders resulting from the reopening of the economy, rather than a real recession. The weeks ahead will indicate which way the scales tilt.

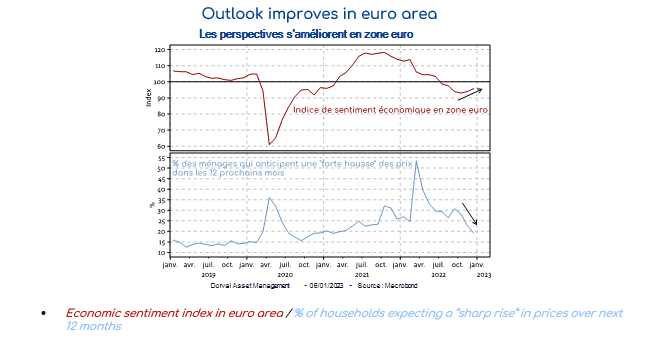

In any case, the theme on the decrease in European risk that we have advanced for several weeks is clearly shored up by recent developments. The prospects of a winter with no major shortages or collapses along with the drop in commodities prices have driven a fresh rebound in economic confidence in December and a sharp decrease in households’ inflationary concerns (cf. chart 3).

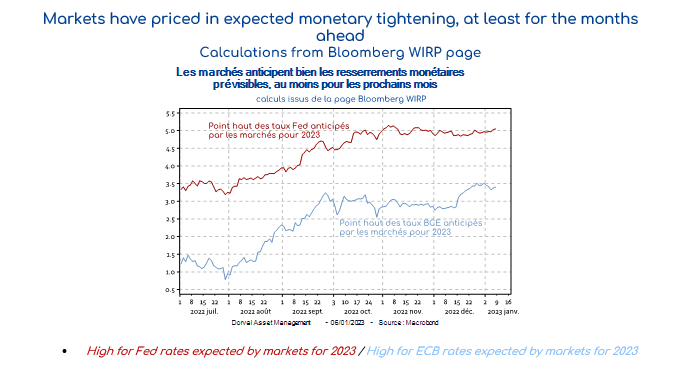

If the resilience scenario is borne out, it does have a flipside i.e. it implies that the Fed and in particular the ECB will continue to hike interest rates to curb inflationary pressure on the labor market. Yet the risks resulting from this tightening are easing as the markets have now priced in the rate hikes that can be expected for the months ahead (cf. chart 4). Rates of 5/5.25% for the Fed and around 3.5% for the ECB broadly equate to the latest indications provided by members of the central banks.

In our international funds, we have increased our equity investment rates by adding to our themes on a decrease in European risk (small-caps, financials) and on emerging markets. We continue to achieve money-market returns by very actively managing the cash component in our portfolios. In our European funds, equity exposure rates are high and beta for our portfolios has been increased over recent weeks.